French Savings and Investment Accounts: Some considerations on the French Plan d’Epargne Actions

It has become a common refrain to say that the European Union requires an increase in investment by retail investors. To that end, on 30 September 2025, the European Commission published a recommendation indicating that “Member States should establish [Savings and Investment Account] frameworks“[1].

Within the European Union, the French Plan d’Epargne Actions (PEA) is the oldest regulated investment account, created in 1992[2]. According to the European Commission, there were 7.3 million PEA Accounts opened in France at the end of 2024, holding around EUR 114 billion in assets.

This is against the backdrop of reports published by the French market supervisor (AMF) indicating that the intention to invest in equities is at its highest level today (30% of French citizens intend to invest in equity in the next 12 months), which is driven primarily by the population that is below 35 years old[3].

On the regulatory side, despite the fact that the French PEA is a well-established product, we have also observed a series of developments: there has been an increase in regulatory scrutiny on industry practices, both in terms of development of new market practices and in terms of supervision and even disciplinary sanctions. Further, we have observed an evolution in the types of actors that seek to propose PEA accounts in France, which has raised both legal and operational questions.

In this context, we set out a very brief overview of the PEA itself: what it is and how it functions (1.), followed by the practical challenges that we have seen, most notably for new actors that seek to enter the French market (2.). Finally, the question may arise how does the regime of the PEA measure up against the benchmark carried out by the European Commission (3.).

1. Brief overview of the Plan d’Epargne Actions: Functioning and Tax Regime

The logic behind the PEA is to favor mid-term investment in French or EU shares.

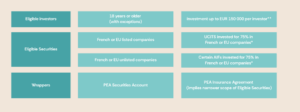

When an investor opens a PEA, he or she can invest in certain eligible securities. If the investor does not make any withdrawals for a period of 5 years starting from the opening of a PEA, he or she will be exempt from French taxes with respect to any dividends received and gains realized upon the sale of those securities[4].

The characteristics of the PEA may be summarized as follows:

*Investment can be direct or synthetic, and can also replicate the performance of indexes.

**For the PEA-PME (dedicated to SME companies), the cap is EUR 225 000

2. Practical considerations for New Entrants and Account Transfers

On the basis of our experience, when certain actors, and notably EU actors that seek to enter on the French market, choose to propose PEA accounts to their investors, this raises the following questions.

| Question | Comment |

| Wrapper | The first question is whether the actor intends to market PEA accounts only as PEA securities accounts or also as PEA insurance contracts.

In this respect, the insurance savings products are an important part of the French investment environment. |

| Operating model | If the actor intends to market PEA insurance contracts, the main question would be to identify insurers with which to sign partnership agreements.

If the actor intends to market PEA securities accounts, then the question arises whether it can provide custody services, or whether it would need to partner with an existing French custodian and merely market their PEA securities accounts. Usually, most French actors marketing PEA accounts do provide custody services; however, this is not the only model. |

| French presence | For EU actors intending to enter on the French market, the question of the French presence is a key question to be asked early on.

In this respect, the PEA custodian will need to submit reports to the French tax administration. Beyond this, there may be an interest in having at least some French-speaking staff to liaise with relevant partners (see below). |

| New clients and incoming transfers | For actors that seek to provide PEA accounts, it is key to understand that many investors already have a PEA. Given that the 5 year delay to benefit from tax exemption on gains starts running from the date of opening of the account, one may open an account and keep it inactive, in order to be able to benefit from the tax advantage if the person chooses to invest in the future.

That means that client acquisition implies assisting investors in transferring their PEA from their traditional account to their new platform. Understanding how client transfers work, both in theory and in practice, is key. Indeed, although there have been significant efforts by the AMF to speed up the transfer of PEA accounts and it has even sanctioned French actors for overly long delays, this remains a serious issue. Case in point, one of the most frequent complaints filed with the AMF mediator is related to transfers of PEA accounts[5]. |

| Securities that the PEA custodian can hold in custody | The AMF has expressly recognized that an actor may open a PEA account, but may limit the types of securities that it can hold in custody (e.g. it may indicate that it accepts only listed securities), provided that it duly informs the client of those restrictions.

However, as client acquisition requires convincing investors to transfer their PEA accounts, this raises the question whether the new PEA custodian can provide custody for all securities that investors may potentially have. For example, if an investor has an unlisted security in his or her PEA account, and the new custodian cannot include such securities in the PEA account, then the investor would not be able to transfer the account unless they sell that security. |

3. EU recommendations on Savings and Investment Accounts

As indicated above, on the basis of the benchmark carried out, the European Commission issued the Recommendation on Increasing the Availability of Savings and Investment Accounts with Simplified and Advantageous Tax Treatment.

Looking to the future, we have set out below a summary of the main recommendations, together with our comments on whether the current PEA account meets those recommendations.

| Key EC Recommendations | Satisfied currently by PEA Accounts? | |

| Each Member State should establish savings and investment account frameworks. | Yes | |

| Member States should ensure that no minimum amount is imposed for the opening of an SIA or for regular payments into it. | Yes | |

| Member States should ensure that all locally authorized financial services providers can offer an SIA. | Yes | |

| Member States should ensure that EU financial services providers (established in another Member State) are not required to comply with additional requirements when offering services together with the provision of an SIA and are able to offer the SIA under the same conditions as locally authorized providers. | Non-French Actors generally establish a French branch[6] | |

| Member States should allow investors to open multiple SIAs including with different providers. | No | |

| Holders of SIAs should not be required to receive financial advice when investing through an SIA. | Yes | |

| Member States should enable the transfer of the portfolio from one SIA provider to another (provided that the receiving SIA provider provides custody services). | Yes, subject to operational challenges | |

| Member States should ensure that SIAs provide access, at a minimum, to the following financial instruments: shares, bonds and shares or units in UCITS. | Bonds are not eligible. | AIFs invested in equity are eligible |

| Member States should encourage providers to offer the widest possible array of investment options available on the market, so that retail investors can diversify their portfolios across asset classes, geographies, issuers, asset managers, financial instrument manufacturers, and risk profiles[7]. | Yes, it being noted that there are also a PEA for SMEs securities and a climate-dedicated savings account | |

| Member States are recommended to introduce tax incentives and ensure that SIAs and assets held in SIAs are given at least the most favourable tax treatment available that is given to income from any asset class or given to an investment product or account.

This may include (i) deductions from the taxable base, (ii) tax exemptions, (iii) tax deferrals or (iv) applying a uniform tax rate to income generated by the SIA. |

The PEA account has a preferential tax treatment.

However, it is not “the most favourable tax treatment available”. |

|

On the basis of the above, while we note that the French PEA satisfies most of the recommendations made by the European Commission on the basis of the best practices identified across the Union, we can still observe certain notable discrepancies.

Given the increase in attention to the PEA, it would be interesting to see whether the EC recommendation would lead to any further changes of the applicable regime.

4. Key Takeaways and Perspectives

The PEA remains a central instrument for retail investment in France, with growing interest from both investors and new market entrants. However, operational challenges—especially regarding account transfers and the custody of certain securities—persist. The increased attention from both French and European authorities may lead to further regulatory developments. Providers considering entry into the French market should anticipate these challenges and ensure transparent communication with clients regarding any restrictions.